Embedded lending for marketplaces: A guide for operators

What is embedded lending for marketplaces?

Embedded lending is business financing built into a marketplace's product interface. Merchants or sellers access capital offers inside the same dashboard where they manage orders without separate applications to external providers.

What separates embedded lending from a conventional business loan is the underwriting model. Instead of financial statements or credit scores, embedded lending uses real-time marketplace data such as sales volume, fulfilment rates, or refund history to set eligibility and terms.

Why are marketplaces well-positioned to offer embedded lending?

Marketplaces already hold the inputs that make financing merchants possible: real-time transaction data, control over the payment flows through which repayment happens, and an established merchant relationship.

-

1.

Real-time transaction data

Marketplaces generate continuous data as a by-product of daily operations: sales volume, fulfilment rates, seasonal patterns, refund history. This is what makes fast, accurate credit decisions possible without building anything new.

-

2.

Control over payment flows

Marketplaces already process merchant payouts, so repayment can happen automatically as a percentage of each sale. No separate billing process needed that creates friction for the merchant.

-

3.

Established merchant relationship

By the time a merchant is eligible for financing, the marketplace has already built a working relationship over months or years. Financing offered through that relationship lands differently than a cold approach from a bank.

How does embedded lending strengthen marketplace supply?

Marketplaces benefit from embedded lending in two ways: it boosts merchant growth and reduces merchant churn.

-

1.

Faster merchant growth

Working capital lets merchants invest in inventory or advertising. According to a study by Forrester, merchants using embedded lending grow 20% faster than unfunded peers.

-

2.

Lower merchant churn

Merchants with active financing churn 70% less than unfunded peers, because the marketplace has not only become part of how they run their business but also a reliable financing partner.

How do marketplaces implement lending?

Marketplaces evaluating embedded lending face a foundational decision: build the capability internally or work with a specialist lending infrastructure provider.

Building internally means obtaining lending licences in each jurisdiction, building underwriting models, arranging capital funding, and managing collections and compliance on an ongoing basis. In regulated markets like the EU, this typically takes 18–24 months and requires substantial upfront capital. The platform also carries credit risk directly.

Partnering with an infrastructure provider moves the licencing, underwriting, compliance, and credit risk to a specialist. The marketplace integrates via API and runs the product under its own brand. The provider handles regulatory requirements across jurisdictions, which is relevant for platforms operating across multiple EU markets where lending rules vary by country.

The tradeoff is control versus speed. Platforms that have built internally tend to be large-scale operations. Platforms that partner are typically prioritising time to market and outsourcing complexity. Most marketplace operators who have launched embedded lending in recent years have done so through infrastructure partners, which reflects the regulatory and operational complexity involved in building the capability from scratch.

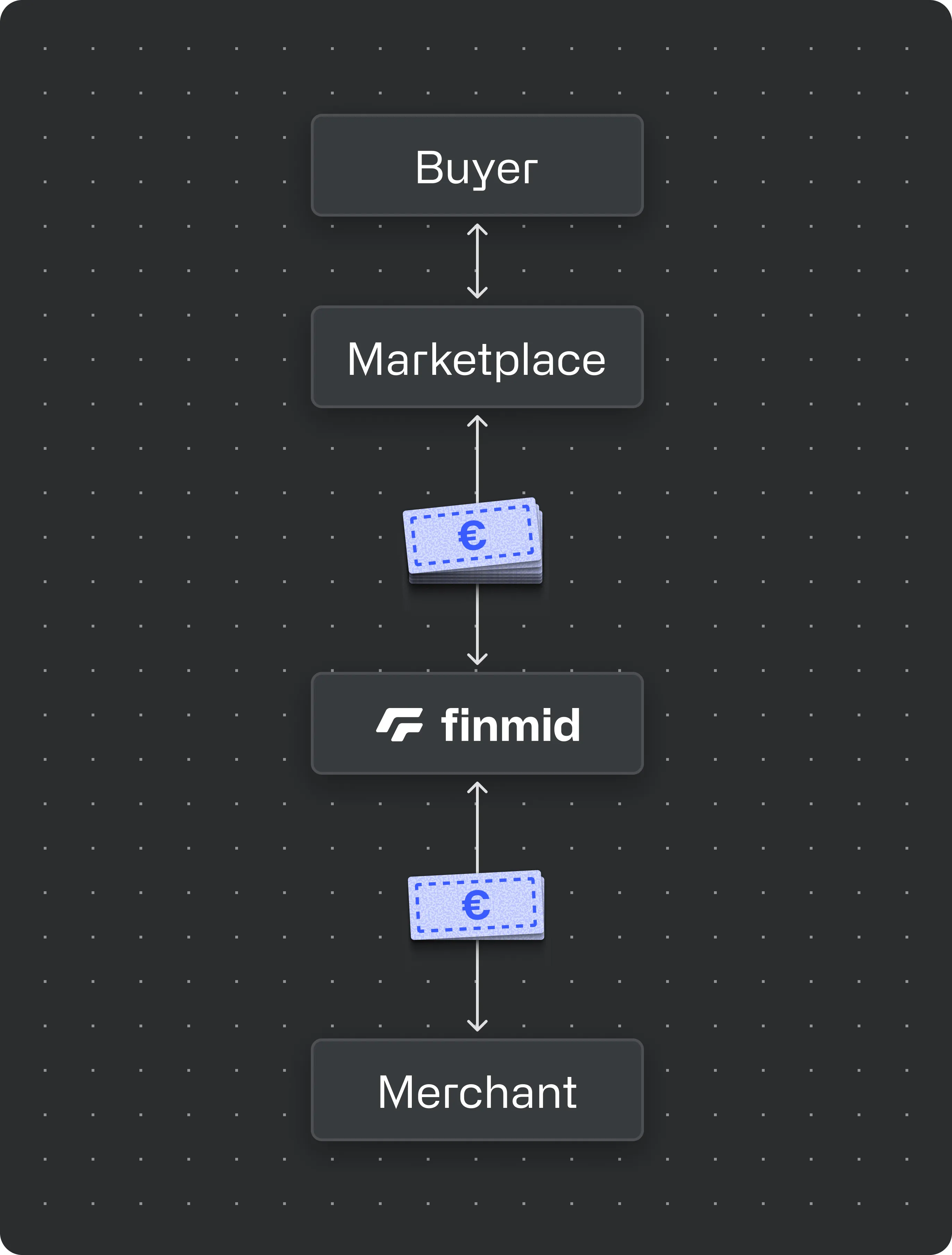

How does embedded lending work, step by step?

When launched with a lending infrastructure partner, embedded lending operates through structured collaboration between the marketplace and the partner. The steps include:

-

1.

The marketplace shares merchant performance data with a lending infrastructure partner.

-

2.

The partner determines eligibility, credit limits, and pricing. Offers update continuously as merchant performance changes.

-

3.

The marketplace displays the pre-approved offer inside the merchant dashboard. No separate application is needed.

-

4.

Repayment is collected as a fixed percentage of sales. No separate billing process is required.

What are the most common embedded lending use cases for marketplace merchants?

E-commerce inventory financing

E-commerce merchants pay for inventory before they generate revenue. This gap widens ahead of peak trading periods like Black Friday when early stock commitments are necessary but the revenue to cover them is still weeks away.

Embedded lending addresses this with flexible credit structures.

Merchants draw against an available limit as needed, pay financing costs only on the amount used, and repay automatically as sales arrive.

For merchants, this means they can stock up before peak seasons, accept larger supplier orders, and avoid stockouts. For the marketplace, funded merchants transact more, list more, and deliver a more reliable buyer experience, which directly impacts GMV.

Hospitality working capital financing

Restaurants and retail stores need to cover equipment maintenance, renovations, or bills whether the month is busy or slow. For restaurants in particular, the gap between when costs land and when a profitable period arrives can stretch across an entire quarter.

Embedded lending gives hospitality operators a working capital buffer that adjusts to actual business conditions.

Revenue-based repayment rises during busy periods and falls during slow ones, which fits the irregular cash flow patterns of food and beverage businesses better than a fixed monthly loan repayment would.

For merchants, this means operational continuity without disrupting the business during slow periods. For the marketplace, an operator that can meet its operating costs processes more orders, cancels less, and stays on the platform longer.

FAQ

Curious to see how embedded lending could work for your platform? Book a demo.

finmid is the embedded lending infrastructure powering platform growth. With its API, finmid enables platforms to launch tailored financing products for their business customers at scale. Across industries, borders, and business models, finmid drives revenue, improves retention, and fuels core business growth. finmid is trusted by Europe’s most ambitious platforms, including Wolt, Delivery Hero, Just Eat Takeaway, Glovo, and FREENOW. Learn more at finmid.com.