Embedded lending explained: A guide for platforms (2026)

What is embedded lending?

Embedded lending is the integration of business financing directly into a third-party platform’s interface, enabling customers to access capital without leaving the platform. Instead of sending customers to external banks or lenders, financing is offered as part of the platform experience.

In this model, lending becomes integrated into the platform’s core workflow. Capital is accessible within the same interface where customers manage sales, payments, operations, or accounting.

Credit decisions are based on platform-generated data such as transaction history, revenue trends, and payment behavior. This approach reduces reliance on traditional bank documentation like financial statements and credit reports.

How does embedded lending work?

Embedded lending operates through a structured collaboration between the platform, the lending infrastructure partner, and the end business borrower. It works the following way:

-

1.

The platform shares relevant performance data with the infrastructure partner. This data supports automated underwriting and risk assessment.

-

2.

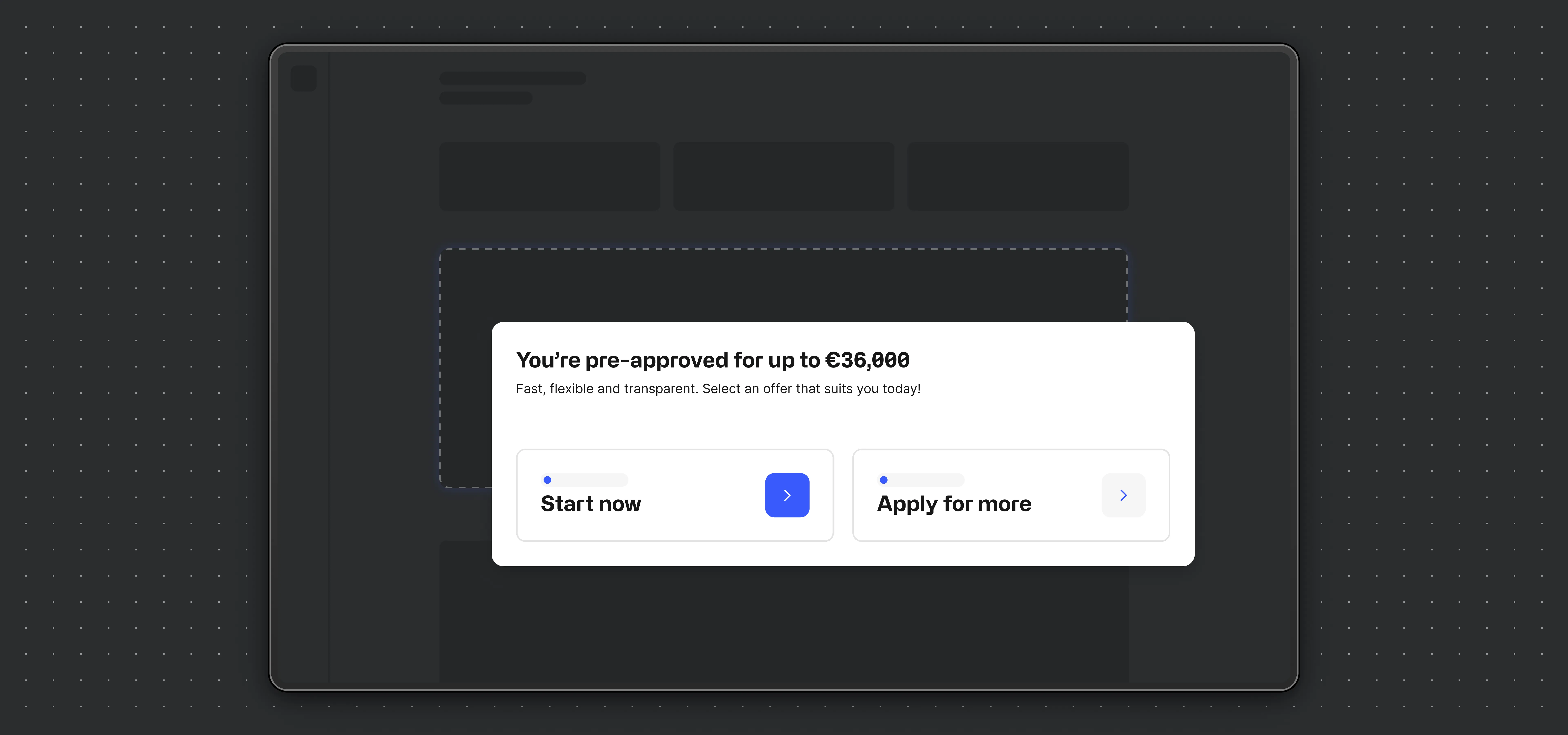

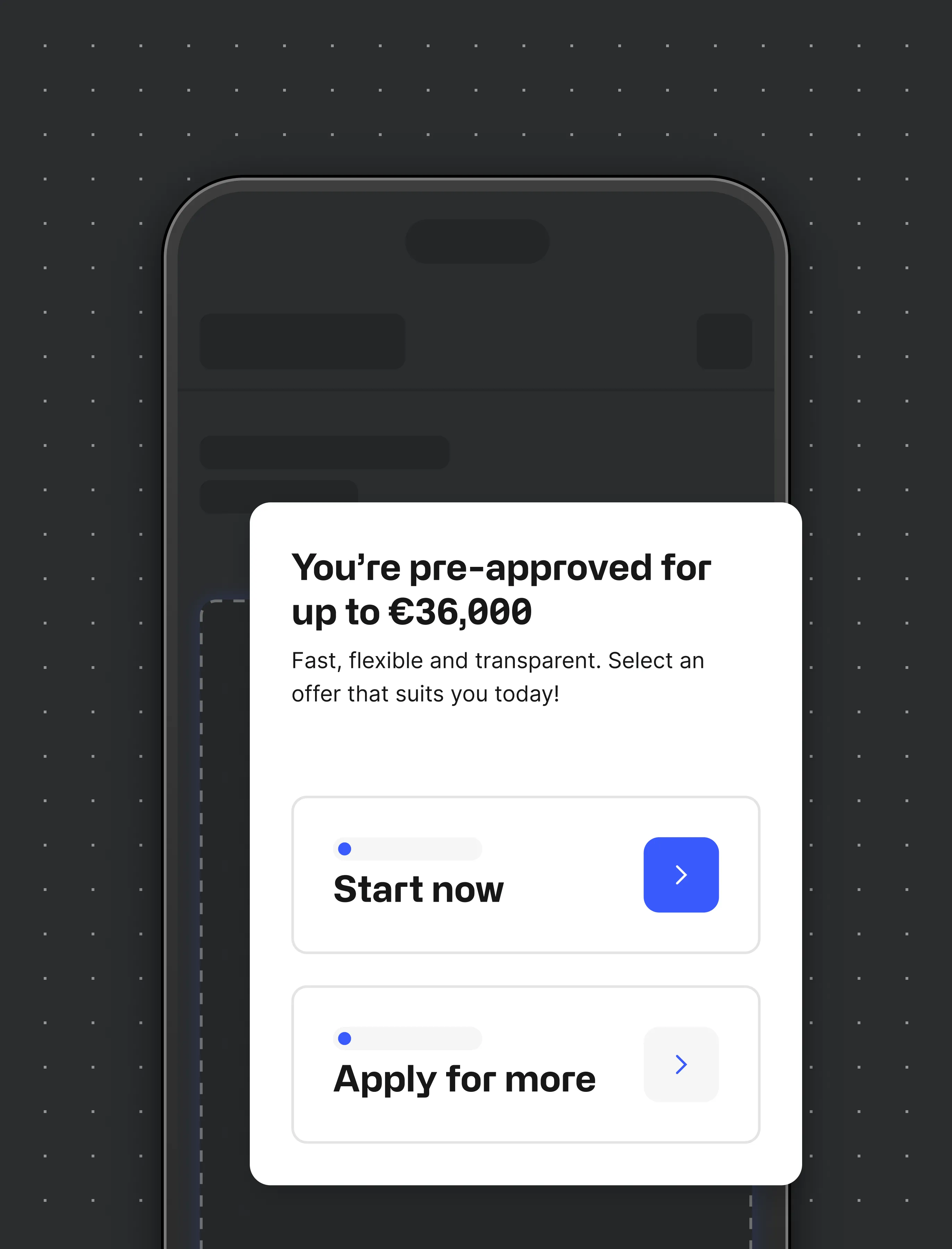

Eligible end businesses receive tailored financing offers directly within the platform interface. Once terms are reviewed and accepted digitally, funds are typically disbursed in up to 48 hours to the business’ account.

-

3.

Repayments are collected automatically via platform’s payment flows or other payment methods, typically as a fixed percentage of future sales.

Who is embedded lending for?

Platforms: Embedded lending is particularly suited for platforms that have visibility into customer performance and recurring transaction data. Examples include:

-

•

E-commerce platforms

-

•

Accounting software providers

-

•

Payment processors

-

•

Vertical SaaS companies

-

•

B2B marketplaces

-

•

ERP systems

These platforms already manage customer workflows and are well positioned to distribute capital efficiently.

Businesses: Embedded lending serves businesses that require growth capital but often encounter friction, delays, or rejection in traditional banking channels. By integrating financing directly into the tools they already use, businesses gain faster and more predictable access to funding across industries.

How does embedded lending benefit platforms?

Embedded lending supports both commercial growth and strategic positioning. The key benefits include:

Accelerated customer growth: Businesses that access financing frequently grow 20% to 50% faster than those without capital support. Increased inventory, marketing spend, or operational investment drives higher activity on the platform.

Incremental revenue streams: Platforms generate additional income through markups or revenue-sharing models tied to financed amounts.

Stronger retention: 64% of marketplaces offering embedded finance solutions report a reduction in customer churn. Access to capital deepens engagement and positions the platform as a long-term growth partner rather than a pure software provider.

Competitive differentiation: By addressing customer capital constraints, platforms strengthen their value proposition. Embedded lending enables smaller businesses to scale more rapidly, increases transaction volumes, and reinforces ecosystem network effects.

What are the risks and challenges?

Below are the most common challenges platforms can encounter when implementing embedded lending:

-

1.

Regulatory requirements

Launching lending capabilities across multiple markets requires licensing, compliance oversight, and ongoing regulatory management. These obligations can be reduced by partnering with an embedded lending provider that assumes regulatory responsibility.

-

2.

Operational execution

Financing programs require coordination across customer support, servicing, and partner management. Gradual rollout strategies and experienced partners can help manage this complexity.

-

3.

Technical integration

Reliable API integration and accurate data synchronization are essential for seamless underwriting, offer generation, and repayment collection. Testing environments and established infrastructure providers reduce implementation risk.

What are the embedded lending use cases?

Commerce marketplace platforms: Commerce and marketplace platforms frequently serve businesses that face barriers to traditional financing. Supporting these customers with embedded lending helps them grow while strengthening the long-term health of the platform itself.

Founded in Finland, Wolt is a hospitality platform that was among the first to embed pre-approved financing directly into its merchant dashboard. Now operating across 20 markets, the program enables merchants to access funding through a seamless three-click onboarding process, receive payouts within minutes, and benefit from transparent, fixed fees. The results speak for themselves: 85% of merchants return for additional financing, and the program maintains an NPS of over 80.

Payment platforms: As payments become increasingly commoditised, many payment providers look to differentiate through value-added services. Lending is a natural extension of the financial stack, allowing providers to move beyond transaction processing and support customer growth more directly.

Sliq, an all-in-one financial management platform based in Cyprus, launched Sliq Boost in partnership with finmid to provide seamless access to financing for its merchants. Eligible businesses can accept pre-approved offers of up to €30,000 in just three taps, with funds available within minutes. Repayments are automatically deducted as a percentage of sales processed through Sliq’s payment network, enabling merchants to manage inventory, equipment upgrades, and seasonal fluctuations with greater ease and flexibility.

How do platforms implement embedded lending?

Implementation is based on three key steps:

-

1.

Choosing to build or buy

Platforms can collaborate with a third-party embedded lending provider, which offers a faster route to market and typically operates through a revenue-sharing model. Alternatively, platforms may build internal lending capabilities, which involves significant investment but provides full control over economics and operations.

-

2.

Defining integration depth

Integration can range from basic referral models to fully white-label API-first solutions embedded directly into the platform interface. Deeper integration requires structured data-sharing and repayment automation, but results in stronger user experience and higher conversion.

-

3.

Designing the go-to-market strategy

Financing offers can be distributed through in-app notifications triggered by performance signals, dashboard placements, targeted email campaigns, or account manager referrals.

Embedded lending remains a powerful growth lever when implemented well. By embedding financing directly into their workflows, platforms can strengthen customer relationships, drive long-term growth, and support users precisely when capital matters most, without becoming a bank themselves.

FAQ

Curious to see how embedded financing could work for your platform? Book a demo.

finmid is the embedded lending infrastructure powering platform growth. With its API, finmid enables platforms to launch tailored financing products for their business customers at scale. Across industries, borders, and business models, finmid drives revenue, improves retention, and fuels core business growth. finmid is trusted by Europe’s most ambitious platforms, including Wolt, Delivery Hero, Just Eat Takeaway, Glovo, and FREENOW. Learn more at finmid.com.