Pre-approved vs. pre-qualified financing offers: which option is best for your platform?

What is a pre-qualified offer?

A pre-qualified offer is an early estimate of funding eligibility. It is typically shown to a large share of merchants before any full eligibility or underwriting checks are completed.

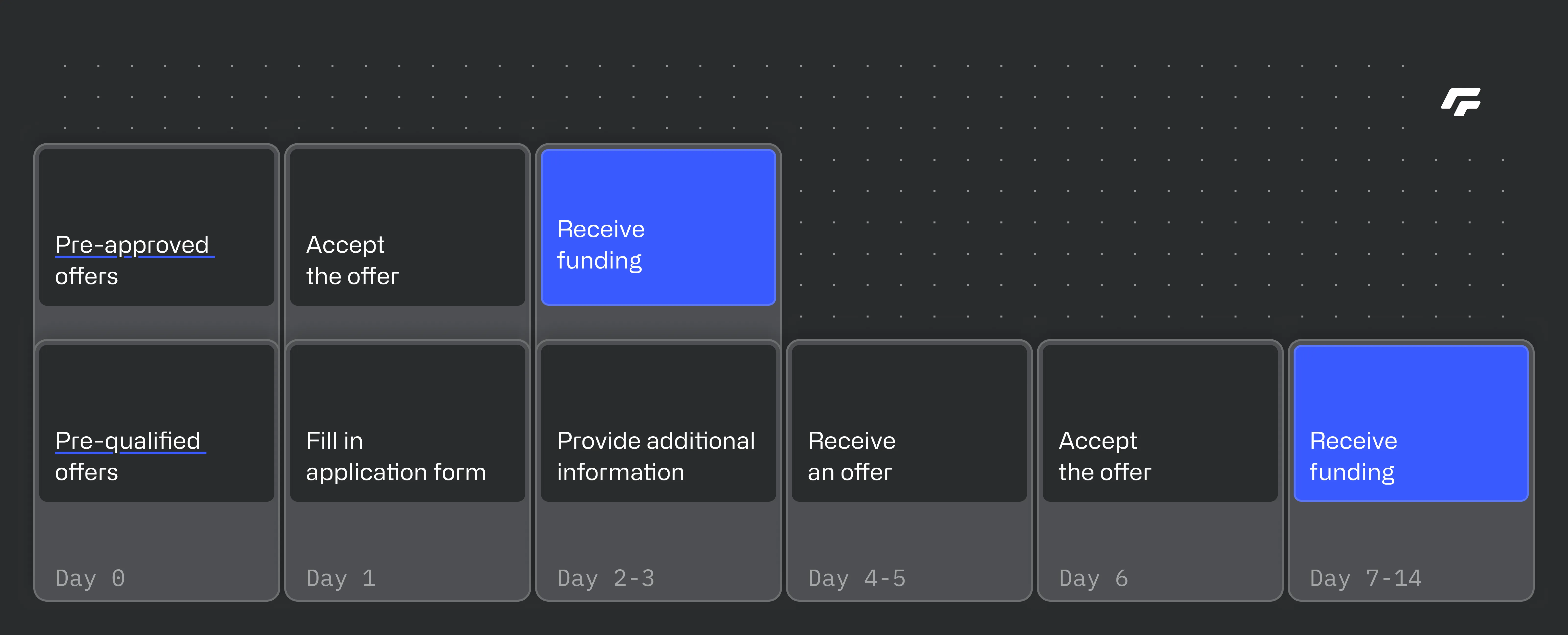

Pre-qualified offers work the following way:

-

1.

Merchant sees an initial offer, often expressed as an "up to" amount

-

2.

They enter a multi-step application flow and submit the necessary documents

-

3.

They wait for the final offer to be issued

-

4.

They receive and accept the offer

-

5.

They receive funds

Because underwriting happens later, pre-qualified offers are indicative by nature. The amount, terms, or eligibility outcome may change once additional checks are completed.

What is a pre-approved offer?

A pre-approved offer is shown only after eligibility and underwriting checks have already been completed. Merchants see confirmed terms rather than estimates.

Pre-approved offers work the following way:

-

1.

Merchant sees a personalised offer with guaranteed amount and terms

-

2.

They enter an acceptance flow and accept the offer

-

3.

They receive funds

Because the assessment happens before the offer is displayed, pre-approved offers provide a guaranteed funding with fewer steps and no surprises.

What is needed to enable pre-approved offers?

Pre-approved offers are based on anonymised merchant performance data. Platforms share this data to enable eligibility checks and underwriting to be completed upfront.

The typical data points include:

-

•

Business founding date

-

•

Business registration date on the platform

-

•

Historical sales performance on the platform

Platforms share the data via API integration or manually depending on the level of integration.

Once an offer is accepted, the platform shares personally identifiable information so that final compliance checks can be performed. These checks are automated and do not require any interaction from the merchant.

How should platforms decide between pre-qualified and pre-approved offers?

Both pre-qualified and pre-approved offers come with benefits and trade-offs. The decision ultimately depends on whether a platform optimises for low effort or certainty and performance.

Pre-qualified offers can make sense if you want to validate demand with low upfront effort and lack consistent performance data. Pre-approved offers are better suited if you want financing to feel native to your product, have strong visibility into merchant performance, and care about delivering a predictable merchant experience.

| Offer type | Benefits | Trade-offs |

|---|---|---|

| Pre-qualified |

|

|

| Pre-approved |

|

|

Pre-qualified

- Low implementation effort

- Faster rollout without data sharing

- Bigger uncertainty and fear of rejection for merchants

- Slower access to funding

- Additional documents required

- Merchant disappointment when offers change or fall through

Pre-approved

- Guaranteed funding

- Faster payouts

- Less paperwork

- Strong UX

- Deeper integration

- Requires data sharing

Why finmid built pre-approved offers

At finmid, we made a deliberate choice to build pre-approved offers exclusively. Our conviction is based on three principles:

-

1.

Funding should be immediate, not conditional

When a merchant accepts an offer, the next step should be payout. Any uncertainty after acceptance slows access to capital and breaks the experience.

-

2.

Uncertainty undermines repeat usage

Merchants do not return to financing products that feel unreliable. Late-stage rejection or changing terms erode confidence quickly.

-

3.

Platforms should only show offers they can stand behind

Showing offers that might change later shifts risk and disappointment onto the platform. Confirmed eligibility and final terms are what make financing feel dependable.

Curious to see how embedded financing could work for your platform? Book a demo.

finmid is the embedded lending infrastructure powering platform growth. With its API, finmid enables platforms to launch tailored financing products for their business customers at scale. Across industries, borders, and business models, finmid drives revenue, improves retention, and fuels core business growth. finmid is trusted by Europe’s most ambitious platforms, including Wolt, Delivery Hero, Just Eat Takeaway, Glovo, and FREENOW. Learn more at finmid.com.