What your lending program’s NPS score is actually telling you

When a platform launches embedded financing, the immediate questions are operational. Did the integration work? Are merchants accepting offers? Is the capital flowing? The question that tends to come later, if it comes at all, is simpler and harder: are merchants actually happy with this?

NPS, or Net Promoter Score, is one way to answer it. It is not the only way, and it has limits. But used well, it tells you something that repayment rates and conversion numbers do not: whether merchants associate the financing experience with your platform positively, or not.

Platforms have different ways to measure merchant satisfaction, and the one finmid has relied on most is NPS. Over time, we have also developed other ways to understand and improve the product experience.

In this post, we explain how NPS works, what our score of above 80 actually means, where the metric has its limits, and what we use alongside it.

What NPS measures

Net Promoter Score is a methodology for measuring how satisfied users are with a product on a scale from -100 to +100. The core question asks how likely a user is to recommend the product to someone else. Respondents who score high are classed as promoters, while those who score low are detractors. The final NPS is calculated by subtracting the share of detractors from the share of promoters.

Promoters - Detractors = NPS

It has become the standard metric for digital product experience because it is simple to collect, easy to track over time, and widely understood across industries. For a financing product, it captures something meaningful: whether the merchant walks away from the experience with more trust in the platform, or less.

How finmid collects NPS, and what a score of 80+ tells us

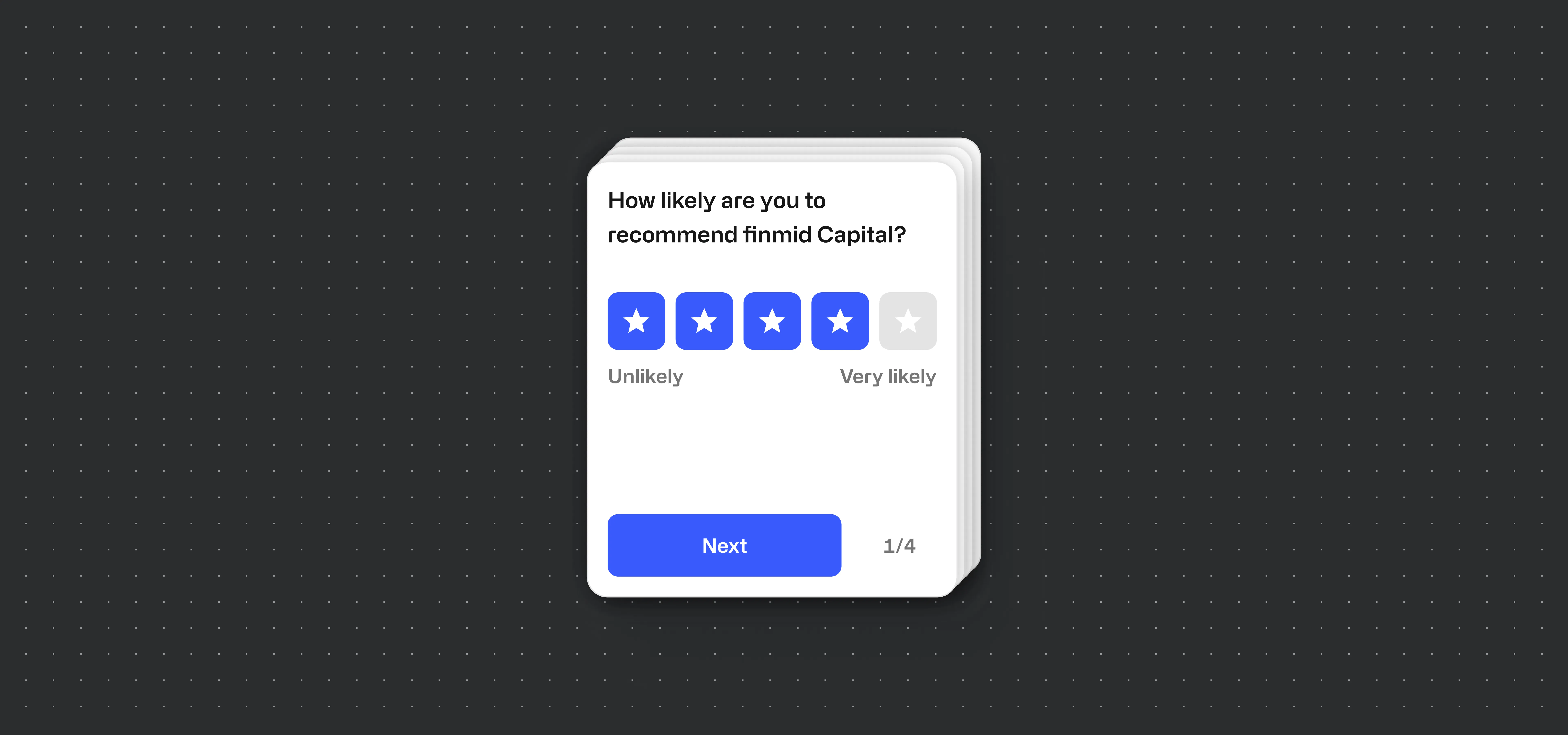

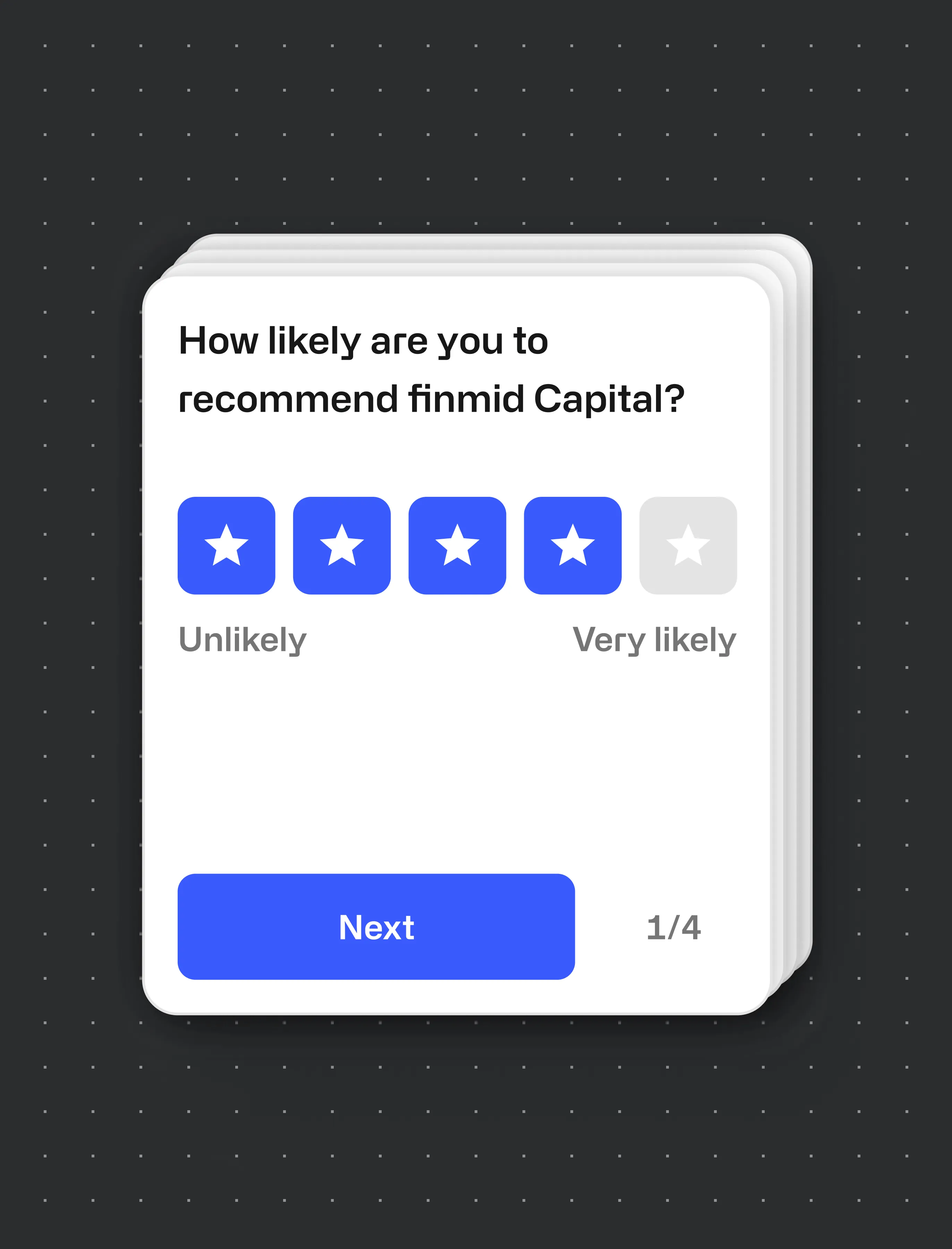

finmid administers the NPS survey directly inside the platform flow. The survey is short: a recommendation question on a 1-to-5 star scale, followed by questions on satisfaction with the offer amount and the overall process.

The results are tracked continuously. On a scale that runs from -100 to +100, scores above 70 are considered excellent across industries, and finmid’s average merchant NPS currently sits above 80. The score, of course, has at times directly influenced product decisions. When scores for an earlier referral-based setup came in significantly lower than the rest of the program, it was one of the factors that led to discontinuing it.

Of course, there is variation across platforms. Scores range from 65 to above 88, depending on, for example, how long the program has been running, what integration method is used or how embedded the experience feels, with fully embedded solutions (data sharing, acceptance flows and repayments) showing significantly higher scores.

For platforms, this matters directly. A financing product that scores well with merchants reflects positively on the platform that offered it.

What NPS does not tell you, and what to do about it

A high NPS confirms the product is working. It does not tell you where or why. For that, the more instructive signal is often the gap – where scores drop and why.

A financing flow with unnecessary friction, extra steps, or a lengthy application process will show up in the numbers before it shows up anywhere else. For platforms, that means NPS is a useful early warning system: if merchants are unhappy with the financing experience, the score will tell you before repayment rates or churn do.

When a merchant rates their experience poorly, finmid and the platform work together to understand what happened. The most common finding is not that the process failed technically, but that the offer amount did not match what the merchant needed. That is a data and underwriting question, and addressing it requires both sides: the platform’s knowledge of its merchants and finmid’s underwriting infrastructure.

To understand merchant experience at a level that a score cannot reach, finmid uses two complementary approaches.

The first is behavioural analytics. Tools that track where merchants drop off in the flow, how long they spend on each screen, where friction occurs, and how they navigate through a session. These surface problems that no survey would catch.

The second is qualitative merchant interviews. A merchant who accepts a 2,500 euro offer when they needed 30,000 euros is not telling you the product is broken. They are telling you something about their business, their cash flow needs, and what a meaningful offer would look like. That kind of context only comes from a direct conversation.

Beyond the score

NPS gives you a number. What you do with it determines whether it is useful. For finmid, the score above 80 validates that embedded financing, done well, creates a positive merchant experience. The low scores, the follow-up calls, the behavioural data, and the merchant interviews are what improve it. A metric is only as good as the system built around it.

Curious to see how embedded lending could work for your platform? Book a demo.

finmid is the embedded lending infrastructure powering platform growth. With its API, finmid enables platforms to launch tailored financing products for their business customers at scale. Across industries, borders, and business models, finmid drives revenue, improves retention, and fuels core business growth. finmid is trusted by Europe’s most ambitious platforms, including Wolt, Delivery Hero, Just Eat Takeaway, Glovo, and FREENOW. Learn more at finmid.com.